The Recession Right Around The Corner

The Recession Right Around The Corner

Every Investor's Worst Nightmare

Here at Simply Finance we give you a high level of Financial Data alongside relatable stories that make it easier for you to learn and make Finance fun.

Let’s put some personality back in Finance.

Don’t be shy to hit the “like” button, share this post, and become a subscriber to this entirely FREE NEWSLETTER if you haven’t done so already!

That’s how we keep the lights on here.

Today’s edition is part of My Stories where I share vulnerable thoughts around my opinions in Finance.

Charts & Chit Chat will be the next edition coming out within a few days where I share Financial Data/Charts alongside quick takeaways that get right to the point.

After that is a weekly Video Post you can think of as a coaching call where I chat about whatever is most relevant over the last week.

For now, let’s get vulnerable.

What’s every investor's worst nightmare?

You know it. It’s the thing that keeps you reading articles like these about men’s underwear sales in decline as you try to figure out what that means for financial markets.

You’re scared you are going to invest at the very top of the market, the day before it all blows up, and then shit your pants just in time for the deep recession to kick in where you won’t have any money left to buy new pairs of underwear.

CNN was right, damnit!!

There’s also the hit on the ego. You don’t want to be the guy or gal that ignored all the signs in front of them playing out one by one, from sausage to lipstick to underwear, and invest at the very top before a big crash comes.

It would suck even more if you were also writing about how a recession around the corner is not likely and publishing those posts on the internet. The proof is all there at that point.

That’s me though. I like to live on the dangerous side I guess, call me crazy.

Last week I chatted about the “starting 5” stock market events that everyone brings up as a reference any time the markets see a down move.

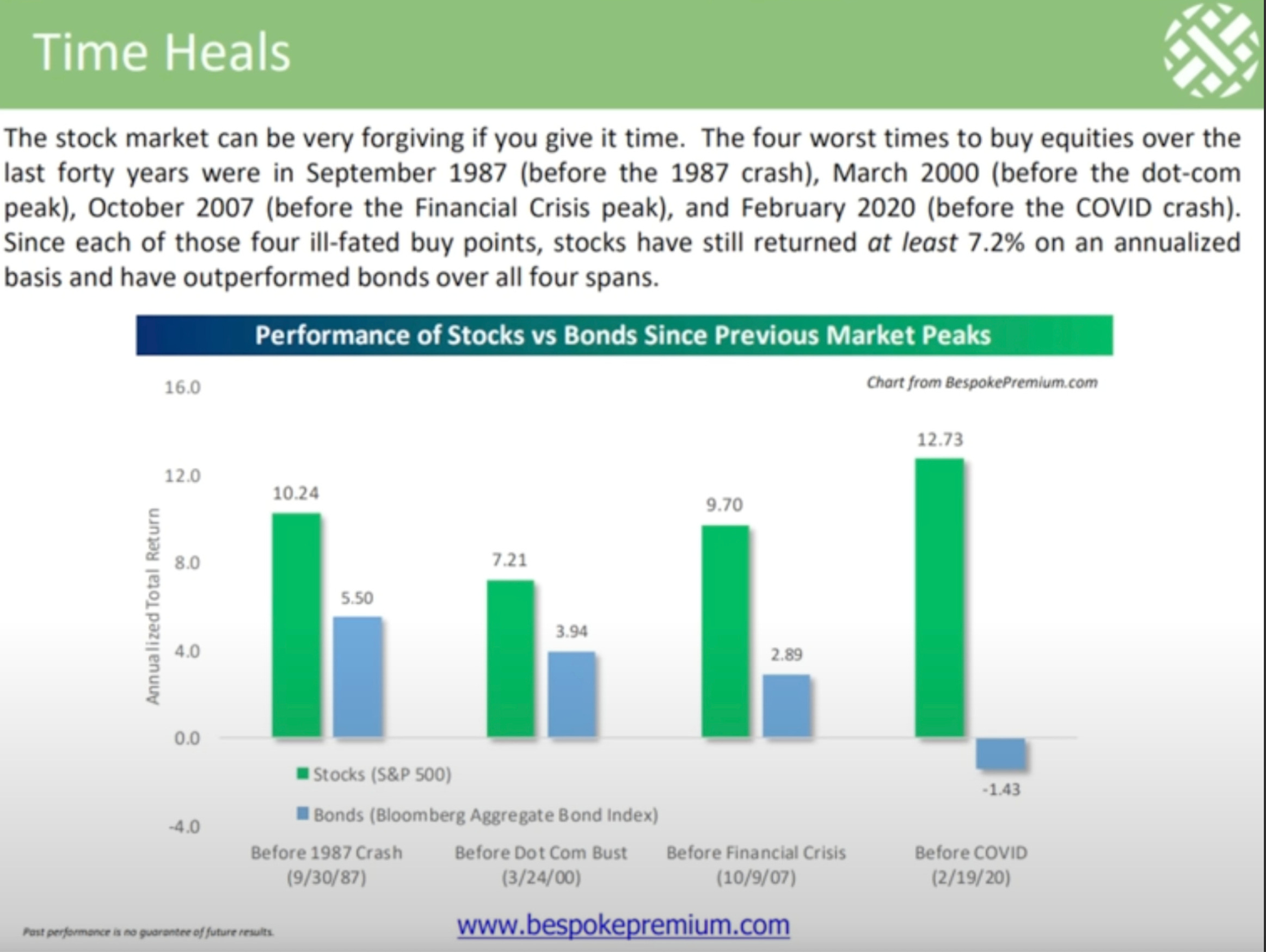

4 of those events are listed in the chart below from Bespoke.

This chart assumes that you invested on the day before each crash started, and plots the annualized returns for both stocks and bonds up until today (2024).

Let’s put emphasis on the stocks (the S&P 500) in the green columns which shows…

Day before 1987 Crash: +10.24% annualized until today.

Day before Dot Com Bubble Burst: +7.21% annualized until today.

Day before Financial Crisis: +9.70% annualized until today.

Day before Covid: +12.73% annualized until today.

Those returns shocked even the permabull in me so I had to double check them myself. I called up my secretary, Chat GPT, and put him to work.

Chat GPT spit out returns within plus/minus 1% of what Bespoke had for each column. They say Chat GPT is only right about 90% of the time, but that’s a heck of a lot more than me during my 3 attempts at pre-calc so we’re in better hands using it than trusting my math.

Bespoke is also a very well known charting company, specifically around Wall Street guys and gals that are managing wealth, and I am jealous of their chart making abilities.

Those figures are accurate, and as I thought about it a bit more it started to make sense. The average return over time for the S&P 500 typically falls within the 7-12% range, depending on what times periods you cherry pick exactly.

This means that most time periods you cherry pick on a chart you can find annualized returns in the 7-12% range. This is especially true the longer the time period is, and that even includes starting at the very top before a “bubble bursts” and the market crashes.

Now of course there are some awful periods of time you can look at too.

Those times are typically short lived and very few and far between though. If anything, they can be looked at as a gift from the market gods allowing you to buy more on a discount.

Find the right perspective.

It’s fair to say the market is trading around all time highs this year so the exit point just happens to be great timing for the returns above. But the market is trading around all times highs a large percentage of the time throughout history and on most years.

In other words, the probability is very high that you will get a chance to sell at some point during all time highs in the market over a 3-10 year period. Historically, new all time highs not being set over a 3-10 year period is very rare.

Most bear markets just don’t last that long.

So you will get a chance to sell positions into strength if you need to.

When you dumb the game down like that it really starts to make a lot more sense, but more so than that it also really takes the agony away.

It eliminates or significantly reduces the fear or being the nimwit who invested the day before the market topped while writing a blog post about how bullish the time we’re in was right before you watched a recession unfold that forced you to wear dirty underwear over the winter months which CNN warned you about just 4 months prior.

That would be one stupid fellow and I sure wouldn’t want to be him.

Dumb the game down though. Accept the uncertainty of market movement, and focus less about why the move is happening and more about what your plan is going to be when certain moves happen.

Dumb it down.

Build up a cash position and scream at the stock chart on your computer screen, “I wish you would fall so I can load up the boat one more time and buy you up” while you knock on wood a few dozen times after that and and make it known to the market gods that you were just playing around and “don’t want no smoke” as the kids say.

Those Jameson shots just get me fired up sometimes.

The thing about the 7-12% returns in the market over time is that they are almost guaranteed if we’re talking about the US Stock market with the US Dollar as the global reserve currency.

7-12% returns over most cherry-picked timeframes in the S&P 500 is about as guaranteed as the “risk free” yield on a US Government Treasury Bond. It’s just the higher returns on the S&P 500 come at the expense of random exogenous shocks on your invested principal over time.

But it’s pretty much sealed and signed. The check is in the mail.

That means that whatever you do in markets you better make sure that you can outpace 10% a year by a percentage amount that is worth the extra work it requires compared with just investing in the index.

Most people are looking for a reason to do something when the better thing would be to just buy and do nothing. It’s very ironic.

10% a year over time is the hurdle rate.

And depending on the perspective you look at it through it could also be the “guaranteed rate.”

It’s good to learn more about Finance and dig deeper than just being a passive investor, but don’t mess up the “guarantee” either. Don’t overthink it. Most importantly, don't bet against it.

Digging deeper into finance typically helps you become a better passive investor too.

As easy as passive investing might sound there are always small ways to improve, like being a passive investor in the asset classes that return more than others, and actually buying low and selling high when you get the chance.

Our job as traders and investors is to find ways to generate returns greater than the 10% guaranteed-hurdle rate, and/or do it in an uncorrelated fashion.

I work for Sky View Trading and our longest and most proven strategy is something we refer to as the “IVL strategy.”

The IVL strategy is pretty boring most of the time, just like being a passive investor is, and that is one reason why I really love it. It’s rarely stressful, just like being a passive investor, and the work is slim to none — especially when we’re talking about it being Automated.

Most importantly, it can and has been profitable in both bull and bear markets with returns greater than 10%.

It likely underperforms the S&P’s when they are up +25% on the year, but it can also return over +20% in a bear market year like 2022 when the S&P’s were down -19%.

This is what contributes to the IVL strategy compounding at a rate greater than 10% annually, and doing so in an uncorrelated fashion from year to year.

Finding just one way to outperform in an uncorrelated fashion is hard. We’ve been able to do it though. We’re in search for that 2nd and 3rd way and we think we have found it.

In the meantime though make sure you don’t mess up a sure thing.

As the old saying goes, a bird in the hand is worth two in the bush.

Or as the kids say now, it’s worth going home with a sure 7 than wasting your time with a doubtful 10.

Remember, it’s all about perspective.

Also remember, optimists make money while pessimists sound smart.

As much as I love Michael Lewis’ book The Big Short, which I actually read before watching the movie on it, one could argue that Michael Lewis and that movie have lost more people more money than anyone in history.

We’ve all tried to be Michael Burry, attempting to nail the top with a bearish trade on the markets that is going to pay BIGLY when a crash comes. We’ve all lost lots of money trying that too, or have underperformed greatly as we lost focus on the long term accumulation of good assets along the way.

If you haven't yet, you're still young in terms of making those type of bets and the key words are "haven't yet."

It’s almost as if we forgot that Michael Burry was paying massive amounts of monthly premiums for years before that bet played out, and that his performance is 1 in a million regardless of that.

Why bet against the sure thing for a 1 in a million chance? It really just boggles my mind.

What do I know though — I’m just a permabull millennial Bitcoin fanboy wearing ripped underwear that’s never traded through a “real bear market,” just a dozen mini ones.

Touché to that argument. We'll see what we get over the next decade I guess.

Maybe I should hedge my bets and go load up on undies while times are still good and I can still stimulate the depressed parts of the economy.

I know the internet is running a sale on tighty whiteys this weekend to spur demand.

I hope you enjoyed reading Simply Finance.

I write a small FREE NEWSLETTER and put out a lot of content. If you enjoy it, the best way to help me out would be to share it with someone else.

And don’t forget to subscribe so you don’t miss the next one!

Disclaimer: These are not recommendations and I am not a financial advisor. These are just my two cents, or two satoshis as the kids say. Remember to do your own homework before making any financial decisions. Also, keep in mind I usually have some personal investments in the things I discuss.

Sometimes those who predict recessions are right.